Every serious company yearns to change. The only way to stay at the top of your industry is to keep producing and keep reinventing yourself along the way.

Sooner or later, everybody else catches up. And that special thing that makes your company different won’t stay special for long.

Which is why innovation isn’t just good, it’s essential. And great innovation management is the difference between organizations that get lucky from time to time, and those that consistently win their markets.

With this guide, you will leave with a clear understanding of what innovation management should look like, and be able to take control of the system of change in your own business.

What is innovation management?

Innovation management is the intentional discipline of making innovation happen. Not waiting and hoping that something brilliant will occur - putting processes in place to ensure that the business makes progress.

And more than just a one-off project, innovation managers build a culture of improvement within the company. By actively encouraging and leading innovation, meaningful change can happen on a regular basis.

This is important, because innovation is often confused with “incredible new products.” Company X is innovative because of all the cool things they build! Which may be partially true.

But more often than not, great innovators have a clear process that brings predictable results. They use frameworks and models to consistently produce valuable products, improve company procedures, and remain ahead of their competition.

It’s this consistency and control over the whole process that you need to strive for.

Why innovation matters

For most businesses, innovation is important to seize a larger market share and stay on top of competitors. If Adidas wants to beat out Nike, it needs to keep reimagining and delivering new sneakers to the market, and give consumers a reason to buy.

But this is rather a limited objective. In fact, perhaps the best reason for companies to innovate is the chance to redefine their market, or find a whole new market altogether. They have the chance to step outside the usual playing field and aim for greener pastures.

And then there’s longevity. The market won’t stay the same forever. Technology, trends, and consumer habits all change constantly, and businesses need to update if they want to keep up.

An unwillingness or inability to innovate can be a death sentence for modern businesses.

Finally, there’s the less sexy reason: constant progression. Companies should want to win around the margins. A small update to a slow or inefficient internal process can make a big difference.

These small steps are innovations too, even if they’re not front page news. If a business can continually improve its project delivery time, reduce the number of meetings, or rebuild specific workflows, productivity can truly soar.

There will also be particular challenges that your company needs to overcome. These could be ambitious growth goals, new demands from customers, or even high staff turnover.

If there is a problem that your current strategies don’t seem to be able to solve, innovation is like the answer.

Key terms to know

There are a lot of concepts and examples to explore below. First, it’s important to clarify the meaning of a few important terms and phrases.

Some of these are used a lot, and a few of them will be brand new to you. But it helps to know what they mean in order to really master innovation management.

Open innovation and co-creation

Traditionally, innovation was a closed-door affair. Companies wanted to brainstorm and build new products in secret.

But this places an artificial limit on new ideas. You can’t possibly employ every smart person out there, and the few people you have can’t possibly think of everything.

So more recently, businesses have begun to embrace open innovation. This involves “active search for new technologies and ideas outside of the firm, also through cooperation with suppliers and competitors, in order to create customer value.” Companies team up to solve issues and encourage submissions from customers, partners, and even competitors.

Co-creation is a similar concept, but usually refers to working specifically with customers or end-users. The company enlists a set group of users to help identify areas for improvement, and then uses this group throughout the product development phase.

A well-run beta test is an example of co-creation, where beta testers take an active role in helping the company perfect its product.

Co-creation makes a lot of sense when you think about it. You’re building products with end-users in mind, so why not let them help you build in the first place?

Continuous improvement and incremental innovation

Continuous improvement is the process of checking work and working methods to make sure that they’re as effective as possible. The more common term in modern business is “optimization.”

This concept is now widespread thanks to popular methodologies like lean, kaizen, and Six Sigma. All of these provide frameworks to help teams review and improve their outputs as they go.

Over time, this results in incremental innovation. Companies make small improvements to products and processes that eventually add up.

This can be more valuable (and certainly more reliable) than the radical or disruptive innovation that many businesses long for.

Radical versus disruptive innovation

It’s tempting to confuse radical innovation with disruptive innovation. Both terms imply that significant change has occurred.

But the difference lies in what kind of change takes place. Radical innovation is "the creation of new knowledge and the commercialization of completely novel ideas or products." In other words, making brand new things.

Disruptive innovation refers to market disruption. Companies either successfully attract market segments that were previously overlooked, or they create whole new markets altogether.

It’s possible to have disruptive innovation without any major technological advance. In this case, there’s no radical innovation. It’s also possible to have major technological or scientific breakthroughs that don’t affect the market at all.

You could come up with the most astounding technology the world has ever seen. But if it doesn’t catch on, it won’t be disruptive.

[We talk about disruption in greater detail below]

Architectural innovation

Architectural innovation changes the way that certain components in a system work together without changing or improving the components themselves.

Computer networks are a good example. Each individual computer hasn’t necessarily changed, but when put together in sequence they create something new and more powerful.

Another simple example is the layout of a hospital. It’s likely more efficient to have the radiology department next to the emergency room for immediate x-rays. Other, less time-sensitive departments can be further away.

When companies are able to piece together components in new and enhanced ways, this is “architectural innovation.”

Innovation portfolio

This concept approaches innovation the same way you’d look at the stock market. You want a diversified portfolio of shares - some low risk (but low return), and others with a small chance of yielding huge gains.

Overall, you have minimal risk and you’ll still make money in the long term.

Likewise, your “innovation portfolio” should be made up lots of small, incremental gains (product updates or process improvements), with some bold game-changers in the mix as well.

If you only have the former, you’re unlikely to separate yourself from the competition. If you only have the latter, you place all your bets on one or two long shots.

Trend scouting

Trend scouting is just as it sounds: uncovering and attempting to preempt the next big industry trends. It’s the reason that companies flock to events like the Consumer Electronics Show (CES) every year, and why the world seems to stop whenever Apple makes a product announcement.

The act of trend scouting typically includes attending events, networking, and a host of other industry research techniques. This can be done by specialized trend scouting teams, or by members of your different business units.

This is a valuable part of innovation management. New trends are often the motivating reason to make major product changes.

And your ability to spot these trends and take action is paramount.

Intrapreneurship

An intrapreneur is “the go-getting business innovator who works within an existing corporate setting, rather than striding out alone to build a business from scratch.”

A company gives its employees the freedom and scope to explore new ideas, and unleashes some of its team’s best qualities.

Fostering intrapreneurship within the company lets your team express their business acumen and instincts without the fear of losing them. You get exciting new developments - hopefully innovations - and they have ownership and sense of achievement.

Management innovation

Although related, management innovation is not to be confused with innovation management. Instead, this concept deals with “anything that substantially alters the way in which the work of management is carried out, or significantly modifies customary organizational forms, and, by so doing, advances organizational goals.”

Put more simply, it asks how can we innovate our management approach?

This specific point of focus can have a huge impact. Management strategy is often very traditional or orthodox, and most large companies follow a similar structure. So when organizations find creative ways to improve management, they have a real advantage over their competitors.

“Over the past 100 years, management innovation, more than any other kind of innovation, has allowed companies to cross new performance thresholds.”

The four types of innovation

In truth, there are probably countless types of innovation. There are also countless different ways to describe the same handful of types, and it’s probably not worth worrying too much about semantics.

But it is important to recognize the broad differences between them. Corporations can become obsessed with one style of problem solving and completely overlook the opportunities to add value across the board.

So to help, we’ll use Greg Satell’s innovation matrix:

Sustaining innovation

As Satell writes, “most of the time we are seeking to get better at what we’re already doing.” In this sense, sustaining innovation is quite similar to incremental innovation (described above).

The main difference between the two terms is mostly just a matter of scale. We think of incremental innovation and continuous improvement as being small, ongoing tweaks. An acquisition, on the other hand, can make a significant change.

But if the company essentially continues what it was already doing - albeit better - we call that a sustaining innovation.

Even most new products actually fall into this category. If you’re serving the same customers with a relatively similar offering, you’re really just continuing as is. Which can be hugely profitable, by the way.

Through specific strategies like roadmaps and acquisitions, companies can improve their existing services without reinventing the wheel.

Breakthrough innovation

Breakthrough innovation is quite the opposite. Sometimes, companies have a particular problem that simply can’t be solved in the usual ways.

Overcoming these issues usually requires a paradigm shift. If a team of developers with established skills can’t defeat a problem, perhaps an artist, philosopher, or dentist can.

This is why open innovation falls into this category in the matrix above. Companies often have to go outside to find breakthrough ideas, because everyone inside the organization has the same way of thinking.

Disruptive innovation

You might commonly confuse disruptive with breakthrough innovation. Many people think of flashy new products as “disruptions,” and the term is thrown about constantly.

But the term as originally coined by Clayton Christensen actually looks almost exclusively at the business model, and not on the quality of the product. In fact, most disruptive companies create products that aren’t good enough for the consumer at the time, and where there isn’t a clear profit to be made.

They build something they’re passionate about, and in time it improves to the point where the mainstream comes to agree with them. For this reason, most successful businesses actually don’t want disruptive innovation. They have a market already and they simply want to serve it better.

The classic example of this is Kodak. The company built the first digital camera in 1975 and continued to invest in the technology into the new millennium. The problem was that Kodak’s primary business was in film and photo printing. If digital cameras took off, they’d detract from Kodak’s main revenue source.

Because it didn’t want to disrupt itself, Kodak never became a true player in digital. And eventually, the digital disruption came anyway. So while Kodak actually had a breakthrough innovation in 1975, it never led to disruption.

Basic research

Satell’s fourth type of innovation arguably isn’t innovation at all. It’s the process that companies take to actively seek out existing scientific research available to them.

They do this by sending scientists and engineers to conferences and having them publish their own white papers. The goal is to bridge the gap between industry and academia.

The reason this is significant for businesses is that so much scientific and technological research is actually public funded. Companies should take advantage of what’s on offer, and should actively encourage their engineers to seek this knowledge.

For example, virtually all of the technology in the iPhone actually comes from previously-existing technology, much of it via the United States government.

Satell argues that basic academic research needs to be a core part of a company’s innovation strategy.

Common frameworks for innovation management

As innovation management progresses, certain methodologies rise to prominence. These are incredibly valuable, because as we’ve already stated, you can’t expect innovation to happen by accident.

You need fonctional ways to guide teams and ensure that new problems are constantly being tackled strategically.

Each of the following frameworks is popular with certain leaders. The one that you choose will depend on the structure of your teams, your resources, and what you’re trying to achieve.

In other words, choose one that makes sense.

Agile

The Agile (or Scrum) method is particularly common among software developers. Teams work in iterative “sprints,” which leaves a set time period available for each phase of a project. Once the time is up, that project phase finishes and it’s on to the next one.

The main benefit of this project management style is the ability to adapt when necessary. Because sprints are short, work is often delivered before it’s complete. Team members or clients then give feedback and changes can be made immediately, rather than waiting for the finished product.

For this reason, companies are more likely to walk away with a product that fits the target market. Designers and developers still get to own their aspects of a project, but the constant feedback loop means that it’s more likely to hit the mark.

Lean start-up

Lean start-up involves many of the same principles as the agile methodology. It “favors experimentation over elaborate planning, customer feedback over intuition, and iterative design over traditional ‘big design up front’ development.”

It’s based on the idea that there’s no perfect business plan, so why try to create one? Instead, it’s better to build, test, and then improve a product.

If you have a problem that needs to be solved, first you build your minimum viable product (MVP) to see if you can solve it. You take this MVP to the market (or beta testers), and from there you discover what’s wrong with it, and if there’s really a market for it in the first place.

The essential premise is that you can’t test a new product if you don’t have a product to test with. So you quickly build something lean, and let the testing begin.

Push versus pull

Push versus pull comes from the manufacturing industry, and it’s a way of visualizing who decides what should come down the assembly line. In a push environment, a production manager forecasts what’s needed and the team begins to create these items.

In a pull environment, the end user (the client) requests an item, and the team begins to build.

For innovation managers, the question becomes does the market tell us what to build, or do we make that decision ourselves? Some companies - Apple, for example - mostly make the decisions themselves. There wasn’t a market clamoring for the iPad - Apple built it and told customers why they needed it.

Other companies rely heavily on open innovation and competitions to decide what to build next. And more often than not, businesses choose a mixture of the two.

Note: This applies on the macro, project level (should we invent an iPad?), but also on the small scale. Innovation teams will fuel themselves with a mix of their own new ideas and requests from colleagues and clients. It’s highly unlikely that a company will rely exclusively on push or pull.

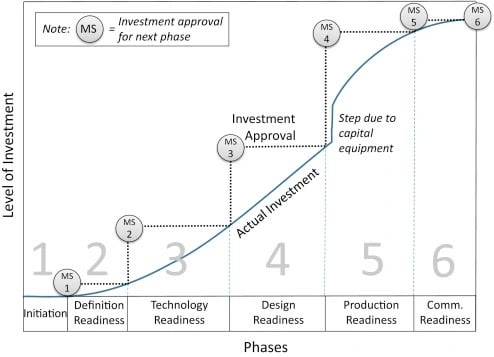

Phase-Gate

This project management framework is particularly common for product innovation. It installs six “phases” through which a project must pass, each with a gate at the end. In order to move on to the next phase, the project must get through the gate and be granted approval:

This method is popular because it limits the company’s investment as it goes. Managers only need to worry about the next round of funding once the current phase has finished. At this point, they’ll be confident that the project is worth investing in further.

But Phase-Gate is often criticized for being too slow. Once a project hits a gate, there isn’t much for the development team to do until the next round of investment is approved.

Unlike Lean start-up or Agile, iteration time can be long and projects are commonly not completed in time. But if the company is confident that the business case is strong and the plan is sound, that extra time can be worth it.

Blue Ocean Strategy

Unlike the other frameworks in this section, Blue Ocean Strategy focuses on the big picture. It’s a way for businesses to conceptualize where they might innovate, rather than the ideation process itself.

Blue Ocean Strategy uses the metaphor of shark-infested waters. These “red oceans” are full of competitors, and the possibility of a company differentiating itself is slim. Instead, companies should find “blue oceans,” free from vicious sharks.

In other words, they need a whole new market.

To do this, they should build a new value curve by answering these four questions:

- Raise: What factors should be raised well above the industry's standard?

- Reduce: What factors were a result of competing against other industries and can be reduced?

- Eliminate: Which factors that the industry has long competed on should be eliminated?

- Create: Which factors should be created that the industry has never offered?

In the process, organizations typically discover that a lot of their behavior is a result of competition. And to truly innovate effectively, it’s better not to try to compete at all, but rather to play a different game.

A 7-step innovation plan

Once you’ve committed and it’s time for transformation, the big problem becomes how to actually make that happen. We’ve already said that your process needs to be repeatable and consistent. So what would that actually look like?

Here’s a good example.

Step 1. Identify a need or problem

To begin, you need to know why you’re embarking on a new innovation project. The good news is that virtually every company has room to improve. New technologies emerge and consumer habits change, and you’re never too far from becoming obsolete. Scary thought.

For a workable innovation strategy, you’ll need a specific problem to solve. Most will immediately begin thinking of wild new product ideas, but it could just as easily be an overhaul of internal processes or a shake-up of management structure.

How to identify problems

Depending on where you’d like to focus your efforts, there are several good places to go for ideas:

- Ask customers. A large survey will give you lots of data, but direct interviews may be a better way to get the details you need.

- Talk to staff. Especially if you want to improve working conditions or create something exciting internally, ask the people with hands-on experience.

- Solicit responses. These could come from staff, customers, or anyone willing to contribute. Creating idea challenges can be a fun way to get everyone invested in the innovation process.

- Study internal data. The jumping-off point may be poor sales in a certain sector, or low staff engagement.

- Watch industry trends. Changing consumer habits industry-wide is another very reason to think about changes you can make.

Once you’ve found a need, you should also set goals or objectives. Aside from solving the problem, what is this project intended to produce? Will it be new products, an updated business model, or something else entirely?

We’re not at the prototyping phase yet, and you don’t even need to have a sketch prepared. Everything is subject to change, so the point is just to have your hypothesis for a solution in place.

Once you have a solid idea of what you’re going to work on, you’re still not done with the assessment phase.

Step 2. Assess the market

Before you hit the ideation stage, it makes sense to test the market. Just because a few people have reported a specific problem, that doesn’t mean that it is in fact an issue generally.

The kinds of questions to ask:

- How widespread is this issue?

- Can it be solved easily with products or processes that already exist?

- Will people actually use (and pay for) a solution?

Again, this doesn’t need to be comprehensive. There will be research and development and product testing to come. You simply need to decide whether this is a project that you ought to pursue.

Step 3. Identify current capabilities

What resources and talent do you have available to you, and what do you need to go out and find? If you already have an established and proven innovation team in place, this assessment may not be too tricky.

But the list of necessities can get long, especially if you’re treading on new ground. For instance, you may choose to go for open innovation and run your first public competition. This requires a whole host of things you may never have thought of:

- A website or mobile app (or both)

- A PR campaign to spread the word

- Prize money and the legal restrictions that come with this

- Rules and regulations to be drafted by legal experts

- An innovation management system to collect and manage submissions

- An assessment team to help judge the submissions. Or a public voting system.

This list isn’t exhaustive, and this is literally just to start accepting ideas! Then you have all the R&D, product development, and eventual requirements for release, all of which are investments on their own.

To be clear, in this step you’re merely trying to figure out if you can innovate in the way you need to. It’s not a question of building prototypes and marketing resources.

One classic mistake that most companies make is over-investing in innovation capacity: “the stuff that’s easy to buy, and that organizations tend to spend too much on: assets and resources. This includes technology and people, as well as tangible, intangible, and financial assets.”

These assets are necessary, but they’re not going to make the biggest difference.

Innovation ability, on the other hand, describes the way that companies create value for consumers through “new customer experiences, a revised service system, or new business models.”

You’ll need both to succeed. But resources and people-power will only get you so far.

Step 4: Generate ideas

Now’s the time to really start thinking about the final product or change you’re hoping to bring about. There are a huge range of ways to find the best ideas, including open innovation and co-creation challenges (described above).

In order to finish with the best possible idea(s), you need to ensure a few things:

- A low barrier for entry. A huge flood of ideas is a scary proposition. But what’s scarier is missing out on the best idea because someone either didn’t want to or couldn’t submit it.

- A clear system for assessment. How will you know which are the best ideas? Whether you create a scoring system or discuss ideas as a panel, it’s important to have this process clear from the beginning.

- An incentive to submit ideas. This is important, but the incentive may not be exactly what you expect. Sure, if you want ideas from the public, a monetary prize helps. But it can be just as powerful to give ownership in some way over the result. Perhaps by letting the public name the new creation, or making the originator part of the project team.

There are of course simpler ways to find innovation ideas. You may simply need to talk to customers or send out a simple survey.

Or perhaps your next great innovation idea will be obvious. You’ve already identified r challenge, and the solution that fits might be clear from the start.

It still pays to go through this process and get as many good ideas as possible. You want to be sure that you’ve done your due diligence before committing.

Step 5: Evaluate and choose the best idea

Once you have a large cache of potential projects, it’s time to choose the right one. As mentioned in the previous step, it’s important to have a consistent and repeated selection exercise.

Cornell professor Samuel Bacharach recommends the following framework:

- Clarity. Ideally you want an idea with “the fewest unknowns.” Just don’t let this become limiting.

- Usability. To what extent does this idea actually solve the problem it’s supposed to?

- Stability. Choose a solution that’s likely to last over time, rather than simply solving a one-time need.

- Scalability. Can the prototype be continued over time without constant improvement?

- Stickiness. Prioritize ideas that can become part of people’s regular routines.

- Integration. Can this idea work within the organization as it exists today? Or will it require significant overhaul?

- Profitability. Obviously this will be important, but Bacharach advises you to think of it as merely one of the seven key considerations above.

If this doesn’t work for you, simply choose the structure you prefer to follow. The important part is to consider ever idea with the same seriousness, using the same framework.

Step 6: Assemble your team

We’re going to talk a lot more shortly about what makes a good innovation squad, and whether you need a dedicated team in the first place.

But what’s certainly true is that you need a dedicated development team, just like you would for any other project.

If you have a whole innovation department, this team will likely be made up of some or all of these players. Otherwise, you’ll need to assign a clear project manager alongside other key contributors. And ideally, they’ll work on this particular project full-time. (More on this shortly).

The team doesn’t have to be large, and it can come from employees who would normally have other responsibilities. But for the life of this project, it’s best if they’re all-in.

Step 7: Create a prototype

Whether or not you choose to follow the lean start-up method, the sooner you can get to a working prototype, the better. It’s incredibly useful to be able to see your idea in action.

More importantly, a prototype lets you determine exactly what are the biggest shortcomings with your project, and where to invest more resources to improve it.

The lean start-up method suggests you not only build this prototype, but get it to market as soon as possible. Even if it’s just in beta, it can really help to let real users test what you’ve built.

Depending on your brand image, this may not work for you. Large, well-known companies have a lot to lose by releasing half-finished products. It may be better to test the prototype internally, and with select focus groups under the condition of secrecy.

But be sure to build something as soon as possible. Then test, evaluate, and iterate.

Minimum Viable Innovation System (MVIS): Another approach

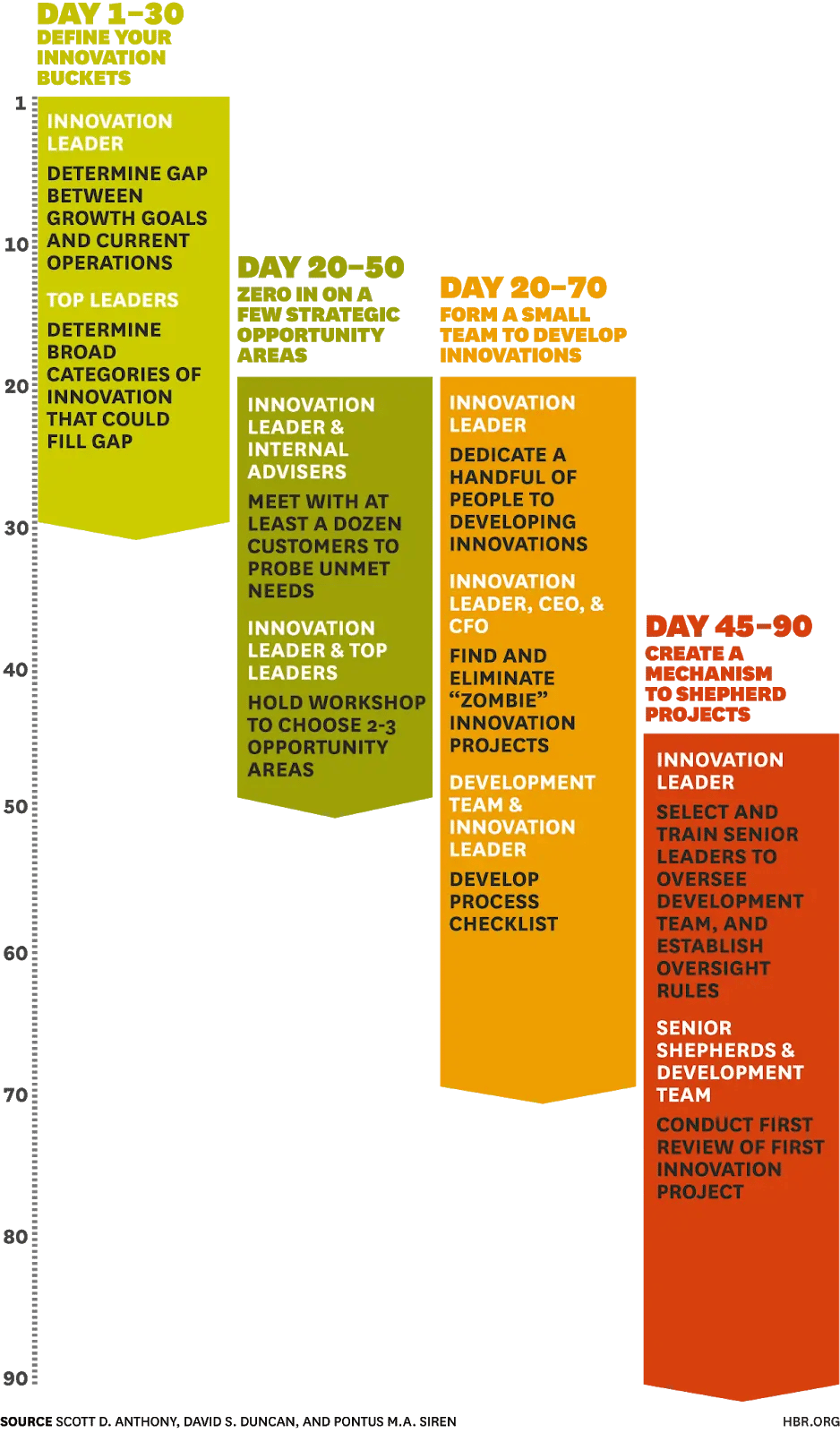

Scott D. Anthony, David S. Duncan and Pontus M.A. Siren offer an alternative strategy. This borrows from lean start-up thinking, and aims to create a sustainable innovation blueprint in the company without turning the whole organization upside-down.

Instead of building a dedicated team, you need one innovation leader (this could be the CIO), and strong buy-in from other senior executives and managers. Together, they discover and shape the opportunities for innovation to the point where they can developed by existing teams.

This is a very attractive model because it requires only “four basic steps in no more than 90 days, with limited investment and without hiring anyone extra.”

Image: HBR.org

Phase 1: Set expectations (days 1-30)

First you need to figure out the kinds of innovation you want to achieve. Based on the gap between your current growth (usually in terms of revenue) and your five-year goals, how significantly do you need to improve?

You then estimate the amount of work that should focus on “core optimization” (improving existing processes and services), and how much should go towards growth from either new markets or new products.

If you can grow at a good enough rate by improving the core, you may not need to think outside this. We want minimum viable innovation, after all.

But if your growth goals are lofty, just the core on its own may not get you there. In this case, it’s time to think outside your current operations.

Phase 2: Find the best opportunities (days 20-50)

Ideally, you should be able to map different innovation opportunities with short- and long-term goals. You might have sophisticated algorithms that highlight specific ways that customers use your products (and your competitors’), predictive financial forecasts, and something else altogether.

But for your MVIS, this is too difficult and time-consuming. You need a quick way to find the best opportunities for innovation projects.

The authors of this strategy suggest something far more simple. Take a handful of executives who’re invested in innovation, and have them talk to at least a dozen customers. Find out what needs are not currently being met.

At the same time, pay attention to suggestions from within the company to see what your employees would change or improve.

Next, lock these executives in a room and don’t let them out until they’ve found three answers to the following:

- A challenge or task that customers have and that isn’t being addressed well

- A product idea that would solve this, or a change in the market that will make this task or challenge far more important

- A reason why your company can solve this better than your competitors

If you have all three of these, you should have a good potential idea. And you want three good potential ideas.

Phase 3: Create your team (days 20-70)

At the same time as these executives are finding opportunities, you need to form an innovation team. These can be sharp members of your existing team or new hires altogether.

The size of the team really depends on the projects you take up. This doesn’t have to be a huge new department - two or three staff will do in many cases.

But one thing is key: they need to be full-time innovators for the length of the project. If you simply sprinkle extra functions around members of your organisation, you won’t get the focus and energy you need.

In the words of the authors, “at least one person (and typically more) [needs to] get up every morning and go to sleep every night thinking about nothing but innovation.”

Phase 4: Build your “shepherding mechanism” (days 45 to 90)

Innovation systems within companies should operate a lot like VCs. You need a committee of senior leadership (much like a VC board) that can assess progress, allocate resources, and stop a project that isn’t working.

Important: This should be made up of executives and senior managers, but it can’t just be your senior leadership team. This group of people needs to think with its “innovation hat” on, and if you stick with your usual set-up they’re likely to fall back on the way business decisions are usually made.

This committee should also operate like VCs:

- They’ll disagree often

- They’ll convene when a decision needs to be made or a when a project is ready for review, but not necessarily on a fixed schedule

- They’ll be able to allocate resources when needed

- They’ll allow project leaders to use resources however they need to (within limits).

After 90 days, you should have a clear framework in place and several projects will be off the ground. Once you’ve seen success in some of these projects, you can take what’s worked and try to formalize it into other processes across the business.

Just like a startup with a successful MVP, it’s time to scale.

How to build an innovation team

Companies with a serious innovation focus will inevitably choose to create a dedicated innovation team or department.

As part of this endeavor, founders and CEOs need to consider the following questions:

- Do you need a Chief Innovation Officer?

- How can you identify and retain talent?

- Will this be a stand-alone department, or will you insert talent and processes into existing teams?

Let’s tackle each of these topics one-by-one.

1. Do you need a Chief Innovation Officer?

Sometimes called “the new CIO” (as opposed to Chief Information Officer), the Chief Innovation Officer role is actually somewhat controversial. A quick search will unearth plenty of scathing headlines:

- Why You Should Eliminate Your Chief Innovation Officer

- Your Company Doesn’t Need a Chief Innovation Officer!

To quickly sum up both of these articles, the arguments against having a CIO look something like this:

- Other senior executives often don’t respect or make space for the CIO

- As a result, the average CIO only stays with a company for two years - not long enough to make real change

- Innovation should be crucial to the roles of CEO, CFO, and CMO anyway, so there may be no need for a CIO

- If one person is in charge of innovation, then theoretically everyone else isn’t. And the whole company needs to see innovation as a central value

These points are all valid. The problem is that numbers 3 and 4 are often missing in most companies. And that’s exactly why a Chief Innovation Officer can be essential to lead the transformation you need.

In a nutshell, your CIO should be “a powerful executive who can counterbalance the natural killing instinct of a company’s business units and design a more innovation-friendly organizational environment.”

The word “powerful” is important. If your CIO doesn’t have authority and command respect, then criticism 1 above is correct. You need someone who other executives will listen to, and who can lead change across the entire organization.

But the decision to bring in a Chief Innovation Officer really depends on two questions:

- Do you truly want to make innovation a core value of your business?

- Can you achieve this without giving one person ultimate responsibility?

If you’ve decided to transform and prioritise innovation, that means that it isn’t happening already. Even if they should be, your executives aren’t currently innovation-focused. Nor are your individual business teams.

And so to make this change, either your executives are going to have to take the responsibility on themselves, or you need to bring someone in. That person’s overarching role is to make sure that innovation is taken seriously, and that the transformation is seen through.

In most cases, existing teams are too dug-in, and they may not see the need for change. Having an impartial observer can help them see that some things are working perfectly, and that there are bigger opportunities waiting to be seized.

Note: You could take lighter steps. Introducing any new C-level executive is big decision, and some companies may prefer to go for a mid-level leader - a Head of Innovation or an Innovation Manager.

Just know that you give the business a smaller chance of success. And Innovation Manager may have wonderful suggestions and the perfect attitude, but without the right authority they can’t always get the buy-in they need from other staff.

You want change from executives and business teams, and to get this you’ll likely need someone they have to respect.

2. How to identify and retain talent

The value of good talent is undeniable. To illustrate, Scott Keller and Mary Meaney put this value in mathematical terms with the example of a three-year project:

“If you took 20 percent of the average talent working on the project and replaced it with great talent, how soon would you achieve the desired impact? If these people were 400 percent more productive, it would take less than two years; if they were 800 percent more productive, it would take less than one. If a competitor used 20 percent more great talent in similar efforts, it would beat you to market even if it started a year or two later.”

So in short, you need the best talent if you want to innovate. And once you’ve found the best people, you absolutely need to keep them.

This is a particularly tricky issue, and the bad news is that there are no quick fixes. Because it depends on culture. Innovative people want to work in an innovative culture.

Most CEOs will tell you that “a great culture” is central to their business. But as Chris Galy asks, “how can ‘culture’ be a competitive advantage if virtually every company says they strive to build a strong company culture powered by customer-focus, innovation, transparency, or any number of other ‘differentiating’ core values?”

In other words, everyone says that their company is unique and that the culture is special. And that’s simply not possible.

Business leaders know this already. 82% of Fortune 500 executives state that their companies don’t recruit highly talented staff.

What do prospective employees actually want?

As stated above, innovative people want to work somewhere innovative. Where their skills are put to use, and where the company believes in them.

So what does a real culture of innovation look like? For one, it’s not based on simple rewards. Rather, “employees who are given the space to focus on learning and development, who work to solve challenging problems, who are involved in company decision-making, and who are provided the opportunity for advancement (among other things), are more likely to stick around.”

And again, it’s easy to say that you do all these things. But you need to actually convince candidates that this is what they’re going to get if they join you.

According to McKinsey, you “employee value proposition” (EVP) needs to be:

- Distinctive. What sets your company apart from all the others? It could be a charismatic founder or CEO, the chance to work on breakthrough technology, or a focus on solving complex challenges.

- Targeted. The top 5% of workers make the biggest difference. So which roles do you need these 5% to fill? If you need elite marketers, your EVP needs to be tailored to them.

- Realistic. The smartest employees will quickly see through your bluster. If you over-promise, they’ll sniff it out immediately. And if they don’t during the interview process, they certainly will after a few months on the job.

These points are also crucial to keeping employees around. If new talent is promised the chance to build exciting new products, they won’t stick around long when they find out that promise was empty.

Overall, the way to keep innovative people around is to innovate. And to make your team members part of that process. The more they can feel new and exciting things happening, and a real push for progression, the more they’ll want to be part of it.

This beats free food and table tennis every time.

3. Do you need a stand-alone innovation team?

The answer to this question is not too different from whether or not you need a CIO. We’ll assume that you know how important innovation is for the business, and that you’re focused on achieving it.

The real question, then, is can you do this with the structure you already have? Or do you need a separate body to push other teams and ensure that innovation happens?

Some of the companies we think of as being quintessentially innovative don’t have a dedicated team. Tesla, for example, gets the most from its teams by having them work cross-functionally with little senior management.

For decades, 3M has given all staff productive daydreaming time - a full 15% of their work day. New ideas can come from anywhere in the company, and this initiative gives everyone the chance to innovate.

But these concepts both rely on an intrinsic culture of innovation. These companies have made innovation central to their very existence. And once again, it’s unlikely that you’re in that position just yet.

To get to that point, you may need to force innovation a little. And a dedicated team may be just what you need.

As we said in a previous section, it doesn’t need to be a big team. But its members do need to be committed to each project. Which means full-time, without too many distractions.

And these teams could come together on a project-by-project basis. This is especially achievable if you have a CIO whose job is to be thinking about innovation non-stop. In that case, this leader can create project teams based on the skills required, as well as choosing managers and setting timelines.

Equally, if you have the resources, you could build a task force with a diverse set of skills that can tackle virtually any challenge put in front of it.

Who should be part of these teams?

Overall, your innovation team should be:

- Mission-driven. Its members should care about the company goals, and truly want to solve the challenges your customers face.

- Psychologically safe. Teams need to be comfortable asking tricky questions, disagreeing with one another, and pushing back against best practices. There will be pressure, and you need innovators who can work under these conditions without nasty clashes.

- Diverse. A wide range of backgrounds and skill sets is the best way to discover unexpected ideas and to approach challenges in novel ways.

- Generous. We might expect innovators to always be mavericks, blazing new trails on their own. But these are teams, and members need to want to achieve things together. Serious egos can be a major issue.

Whether you pluck these people from your existing employees or hire from outside is really just a question of resources. As long as they’re able to work independently with a singular focus on each challenge, they have a good chance of success.

How to measure innovation

Business leaders rely on measurement. They need to know empirically whether every project was a success, and what the return on investment is.

This way, they ensure they’re making the best possible decisions and approving projects that are likely to succeed.

With something as complex and often unpredictable as innovation, this philosophy becomes tricky. Some business leaders will only greenlight a project if they think that a quality return is inevitable.

It’s fairly easy to measure the direct outcome of a new product or service. You can calculate the resources that went in and the revenue that came back - voilà. But it’s harder to assess incremental innovation which can impact all areas of your business. And what about if your goal is to foster innovation throughout the company?

Let’s examine some of the key methods businesses have to measure their innovation efforts.

Overall innovation metrics

Before looking at key performance indicators, we need to start with a general distinction: input versus output metrics. These are the two main categories into which all of our other metrics will fall.

Input metrics

As the name suggests, input metrics look at what you put into innovation. How much time, money, and people power do you dedicate to each new project or goal?

Especially when you’re building a new innovation strategy, these are hugely important because they’re the easiest to control. You decide how much to invest, and then you measure whether you achieve that level of investment, go beyond it, or come up short.

Output metrics

Output metrics help you measure the results of a campaign or project. These can be revenue from sales or the number of units sold. They can also include internal measurements like the time saved on a particular task, or improvements to scores on employee tests.

Naturally, both input and output metrics should match the goals of a particular innovation project.

With that clarification out of the way, let’s look at some of the most common ways that businesses measure innovation.

Key performance indicators

Every company will have its own precise metrics. It’s up to you to identify what these are for your business.

But here are the general KPI categories to think about.

Timesheet metrics

We mentioned above that 3M designates 15% of each employee’s time to active daydreaming and creative thought. Google stepped that number up to 20%.

Your first thought when you read that was probably sure, but I bet they never actually use this time. Everyone’s always too busy and there are more urgent things to work on.

Maybe. Google and 3M executives could pretty easily find out. Plenty of companies use timesheets, and all it takes is a specific time code for “creative thinking” or whatever they choose to call it.

Timesheets give us easy innovation input metrics. You can literally see exactly how many people hours are being put towards new projects, enacting changes, or simple creative thought.

Especially if your goal is to make innovation a core principle throughout the business, it may be necessary to make sure that people actually assign real working hours to it every single week.

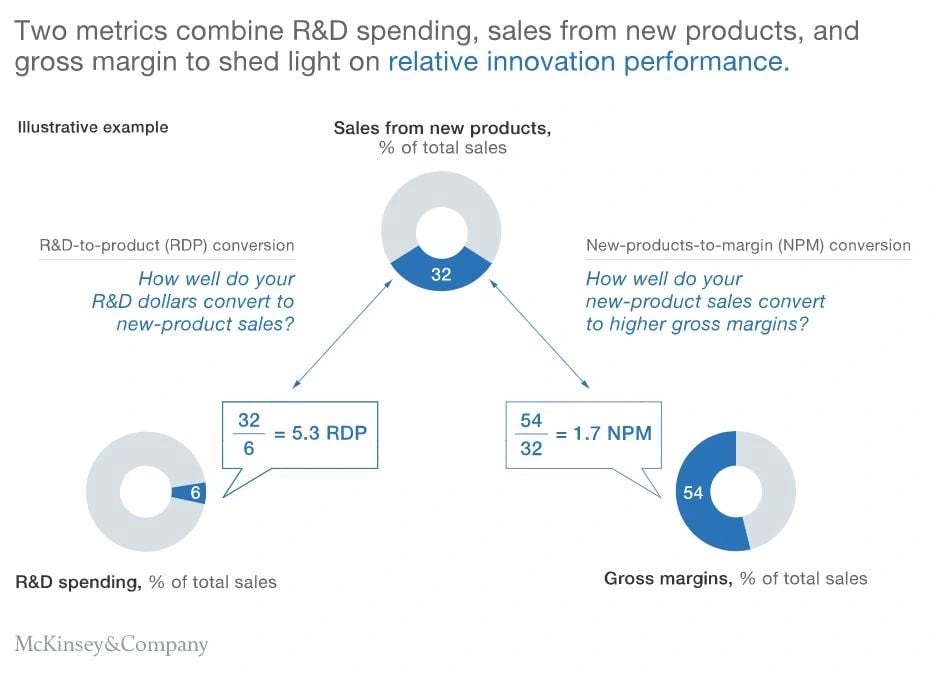

New product metrics

In many cases, innovation projects will lead to new products and services. Thus, you can measure the output of these projects by tracking a few metrics associated with the products yielded.

For starters, it’s helpful to see how sales and revenue compare with your other services. A new product might leap immediately to popularity and bring with it a new and rich revenue stream.

But out of context, these numbers can be misleading. Which is why McKinsey recommends that you measure new product sales against the development costs that went into them, as well as to gross margins. And all of these numbers should be taken as a percentage of total sales:

Source: McKinsey & Company

This way you measure the value of new innovations against what would have been produced if you’d continued with the status quo.

Financial metrics

The financial figures in this section are another example of input metrics. What do you invest financially into innovation?

For example:

- How does each innovation team use its budget (does it under- or overspend)?

- What does the company invest in innovation as a proportion of total company spending?

- How much does the company spend on mergers and acquisitions as a way to spur innovation?

It’s worth noting that plenty of new products take time to become profitable. Relying too heavily on these kinds of financial metrics can cause executives and boards of trustees to become anxious.

But these measurements can help to ensure that you’re actually investing what you planned to. If teams are regularly coming in under-budget, but also not producing what you’d hoped, this might be the perfect place to take action.

Training and staff competency metrics

As we’ve seen several times above, education and training are a smart and necessary way to foster innovation and keep stay happy for longer. And these are measurable investments for business leaders to take into account.

It shouldn’t be hard to track:

- Allowances given to employees for outside study

- Costs associated with bringing in educators and hosting seminars

- Courses completed and even improving test scores (where appropriate)

It’s also worth assessing staff satisfaction with the level of education they receive on a regular basis. Do the extra trainings line up with improving satisfaction scores?

The flow-on effect can be staff who stay with the company longer, and who’re more productive due to the contentment they feel at work.

Management and leadership metrics

Innovation usually relies on significant buy-in from management. Senior executives, especially, need to believe in this vision and commit to making change happen.

And we do have some metrics to help measure whether this actually occurs:

- The number of projects that each senior manager or executive leads or sponsors

- The committees and challenges they oversee

- The amount of time spent by each on these projects

- The major market innovations each manager is able to stimulate

Not every senior leader is going to have the same level of interest and commitment to the cause. And that’s exactly why it can help to assign these managers specific innovation KPIs.

Because if there’s one thing executives understand, it’s measurables.

Successful innovation examples

We’ve looked at a lot of innovation management concepts so far. And while we’ve seen examples sprinkled in, most of this post has dealt with theories and concepts rather than real-life cases.

In this section, we’re going to look at several quite different cases of companies with successful innovation strategies. Each highlights a particular aspect done well, and should give you some good ideas to work with.

NASA - a new business model

NASA is an excellent example of a company (or in this case a governmental agency) innovating its business model to ensure its own survival.

Soon after the moon landing in 1969, NASA’s budget fell sharply (as a percentage of the American federal budget).

Over the decades that followed, the concept of “commercial space” emerged. Private companies began developing new technologies, and NASA no longer had a monopoly on extra-terrestrial travel (in the USA).

The agency had to go from the exclusive inventor of some of the most inspiring technologies of all time, to a collaborator. From 2006 onwards, it’s been following the network model, in which many important facets of its missions are contracted out to new players on the scene.

Some of these companies can produce what NASA needs faster and cheaper than the agency can. And with a sometimes alarming budget cuts, these public-private partnerships have helped keep an iconic brand alive and well.

Unilever - co-creation with customers

With over 2.5 billion users of its wide range of products, Unilever has a large pool of customers to mine for ideas. And it does so on a regular basis.

The giant corporation launched an Open Innovation portal in 2010, which puts challenges to the public and lets them be part of the ideation process.

The subjects range from smart packaging ideas, to more efficient materials to be used in products, to clever new ways to freeze goods.

The platform is open to anyone, including established businesses or university researchers, as well as people developing in their own garages.

The result is a fast and democratic way to generate a lot of potential ideas.

Google Wave - a useful failure

Most wouldn’t consider Google Wave to be an example of success. After all, Google’s leadership suspended the project in August 2010, only three months after its public release.

In the company’s own words, Wave was “equal parts conversation and document.” Multiple users could read and edit documents at the same time, as well as communicating in a manner similar to email:

But it didn’t last long, and the product is no longer available.

So why is this a good example of innovation? Because as Karim Lakhani wrote at the time:

“Even a company like Google, recognized for its wealth of intellectual talent in its employees, was not able to figure out beforehand if there would be a market for Wave. Google should be applauded and rewarded for pioneering a risky project and publicly launching it so that it can learn from the market.”

Innovation always comes with a risk of failure. And Google Wave aimed to overhaul the way web users communicated completely. Users and journalists were hugely excited about the possibilities at the time.

In other words, it was a good idea. And many of the functionalities built in the process are still used across the web today.

But upon release, it clearly didn’t have the market that Google had hoped. So the company pulled the plug.

This embrace of failure is one of the reasons that Google is so successful. It build Google Labs (Wave was a Labs product) for this exact reason: “In contrast to a typical corporate environment, where failures can cost a company millions (or worse yet, a brand), a Labs setting values successes and failures equally.”

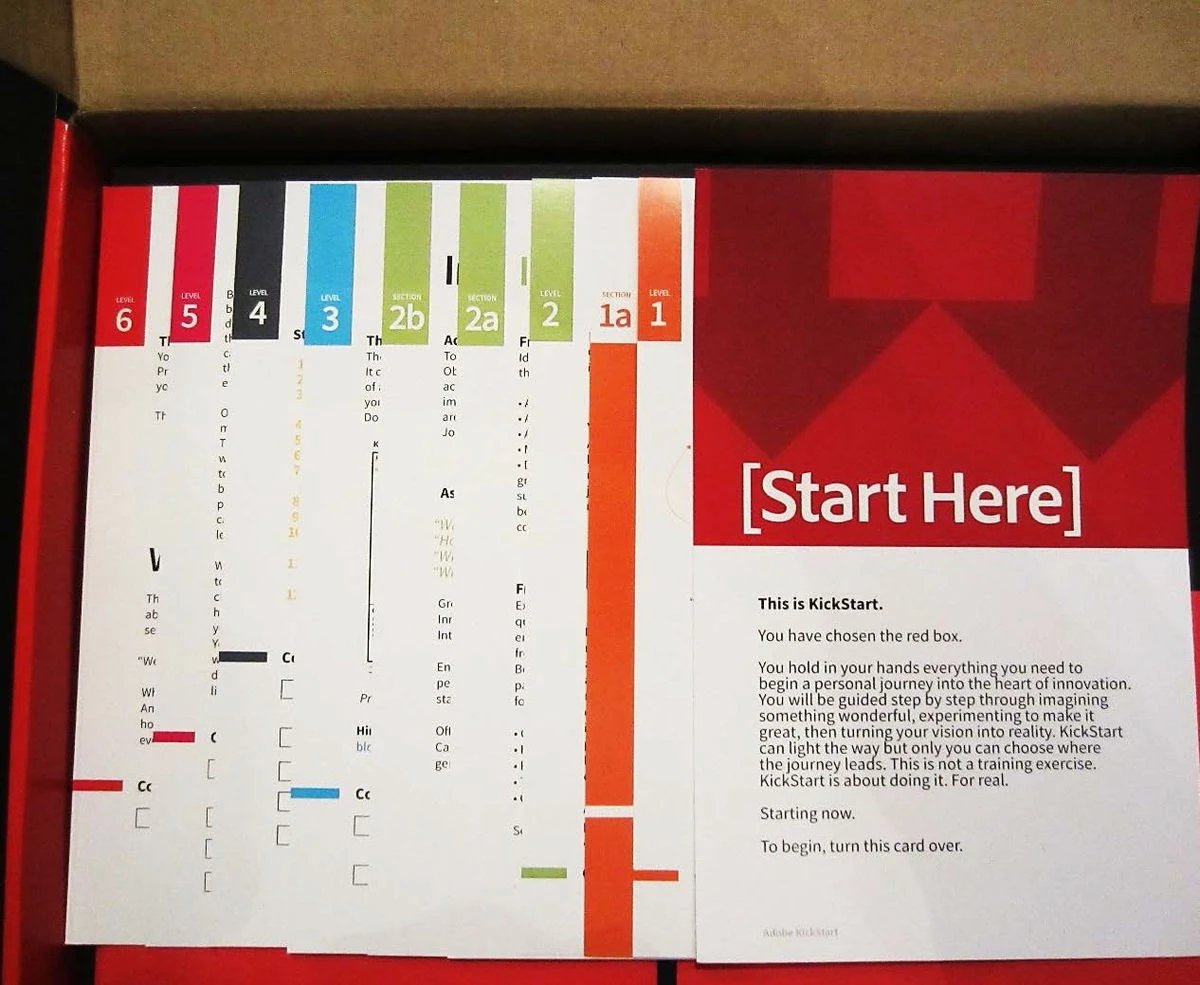

Adobe Kickbox - intrapreneurship

A lot of companies talk the talk about encouraging intrapreneurship and letting employees create. Adobe definitely walks the walk.

The Kickbox program lets an employee take a prepaid $1,000 credit card and create a prototype. The card comes in the “red box,” which also includes a process to follow to actually build the idea. And the employee is encouraged to ask for help and mentorship along the way.

Once the prototype is ready, said employee can pitch it to any (or all) of 10 executives. If just one of these 10 buys in, the employee is given “the blue box” - which means the company will actually take up the idea.

$1,000 may seem like a lot to give out willy nilly, but it’s not really in the long run. If just one out of every 100 prototypes is a hit, that’s a $100,000 prototype. Most companies would spend far more than that on new product ideas.

Where to begin

This article has explored the biggest innovation management strategies, theories, and challenges facing businesses today. If you’re about to embark on building a whole new program for your business, these are important concepts to understand.

But now comes the tricky part: putting these ideas into action.

As we’ve seen time and again, your success depends on a few things:

- The firm belief that innovation is essential to your business

- True buy-in from executives and senior leaders

- The ability to find and keep good talent around you

- Smart, repeatable processes to identify opportunities and create new products

A lot of companies struggle with that last point. There are many different frameworks and models to choose from, and you likely don’t have established processes to rely on.

If this is the case, a good innovation management system can help. These tools give your whole team a structure to work within, including easy ways to find and test new ideas, brainstorm effectively, and track projects as they progress.

In short, the right tool will guide you through the innovation process from start to finish.

To learn more about how Braineet can do exactly that for your business, book a demo with our expert innovators now.